Development

Research

Jun 3, 2025

9 min read

summary

FinTech onboarding is not just a functional gateway — it’s the moment where design, psychology, legal compliance, and business KPIs intersect.

In the FinTech world, trust is everything — and it starts in the first 30 seconds. Your product may offer industry-leading features, seamless transfers, or the best exchange rates, but if your onboarding is slow, confusing, or feels untrustworthy, users will churn before they ever experience your core value.

FinTech onboarding is not just a functional gateway — it’s the moment where design, psychology, legal compliance, and business KPIs intersect. And user experience (UX) is the glue holding it all together.

In this article, we’ll explore:

- The financial cost of poor onboarding

- The most common types of onboarding in fintech apps

- Actionable UX strategies that turn onboarding from a blocker into a growth driver

The real cost of poor onboarding

FinTech companies invest significant resources in customer acquisition, often spending hundreds of dollars per user on ads, content marketing, SEO, referral programs, and incentives.

However, according to a 2022 report by Signicat, the average onboarding drop-off rate in FinTech is 63%.[1] In other words, more than half of acquired users never even finish signing up.

This high abandonment rate translates into substantial financial losses. Signicat’s research estimated that around 120 million new bank accounts are opened across Europe each year, and with a 63% abandonment rate, approximately €5.7 billion is wasted annually on incomplete onboarding processes [2].

Before we dive into the cost of poor onboarding, it’s important to understand that not all onboarding flows are the same. In FinTech, onboarding can include several distinct types depending on the product’s purpose, legal requirements, and user goals.

Why users drop off:

- Overly complex forms

- Lack of feedback or progress indicators

- Poor mobile optimization

- Mistrust of sensitive data collection

- Requiring identity verification too early without context

Let’s break down the 3 most common types of onboarding in FinTech apps — and show how to fix what’s usually broken.

KYC Onboarding – Identity Verification

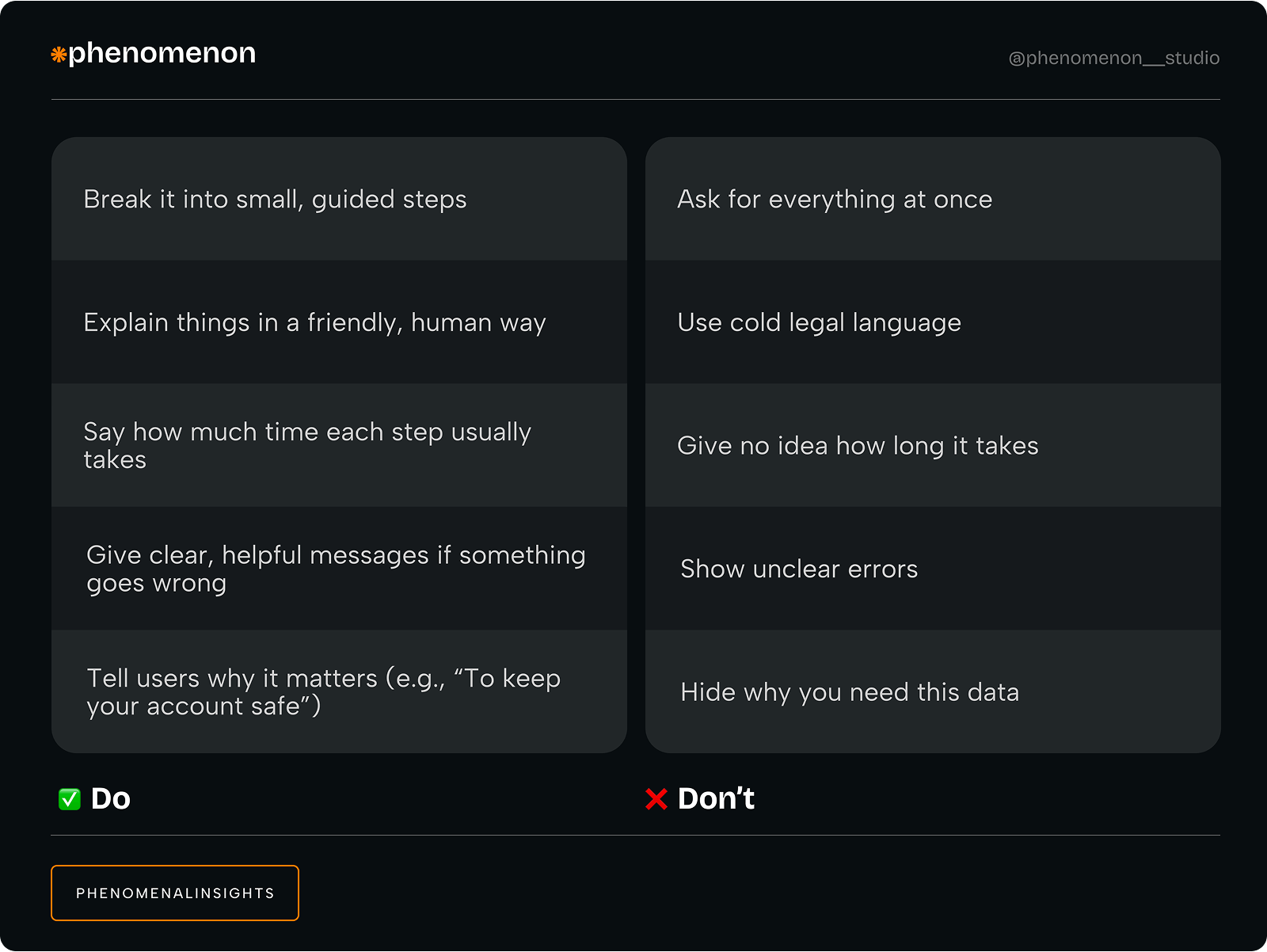

KYC (know your customer) is a mandatory process used by financial institutions to verify the identity of their users and prevent fraud, money laundering, or terrorist financing [3].

Common KYC steps include:

- Providing full name, address, date of birth

- Uploading government-issued ID (passport, driver’s license)

- Taking a selfie or video for facial verification

- Proof of address (e.g., utility bill)

Today, most teams integrate third-party KYC providers because this cuts down development time and ensures legal compliance. But even if KYC is external, the user still goes through your interface. The design experience still matters.

Our case

In a recent project, our team redesigned the onboarding for a mobile wallet with Solana integration. Their KYC drop-off rate was 62%. Users were abandoning the process at the document upload stage.

What we did:

- Replaced the 5-step KYC form with a step-by-step wizard and visual progress bar

- Added microcopy like “Takes less than 2 minutes”

- Used real-time photo validation

- Created illustrations and short explanations for each step

Results:

- Drop-off decreased from 62% → 27%

- Onboarding time reduced from 4.5 minutes → 1.9 minutes

- Verified user conversion rate rose by 38%

This directly impacted revenue, because verified users had higher deposit and transaction volume.

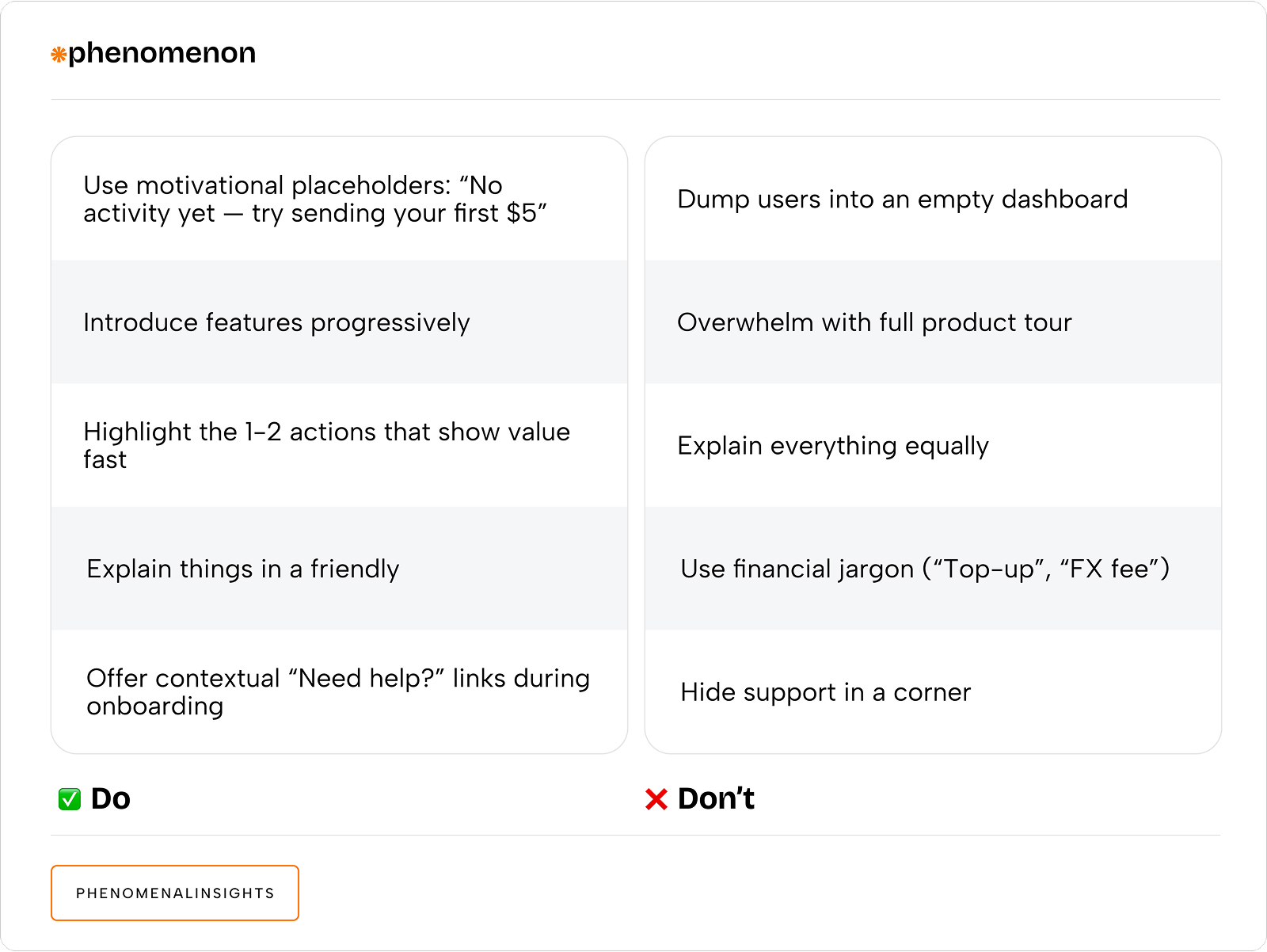

Feature Onboarding – Reaching First Value

Most FinTech users churn before they experience your product’s real value. Feature onboarding helps them take their first meaningful action:

- Send their first $10

- Set up savings

- Order their card

Real-case impact

In a wallet app, we noticed that 30% of users never completed their first transaction. By redesigning the empty dashboard state and adding a friendly prompt, we increased activation to 67% in just 3 weeks.

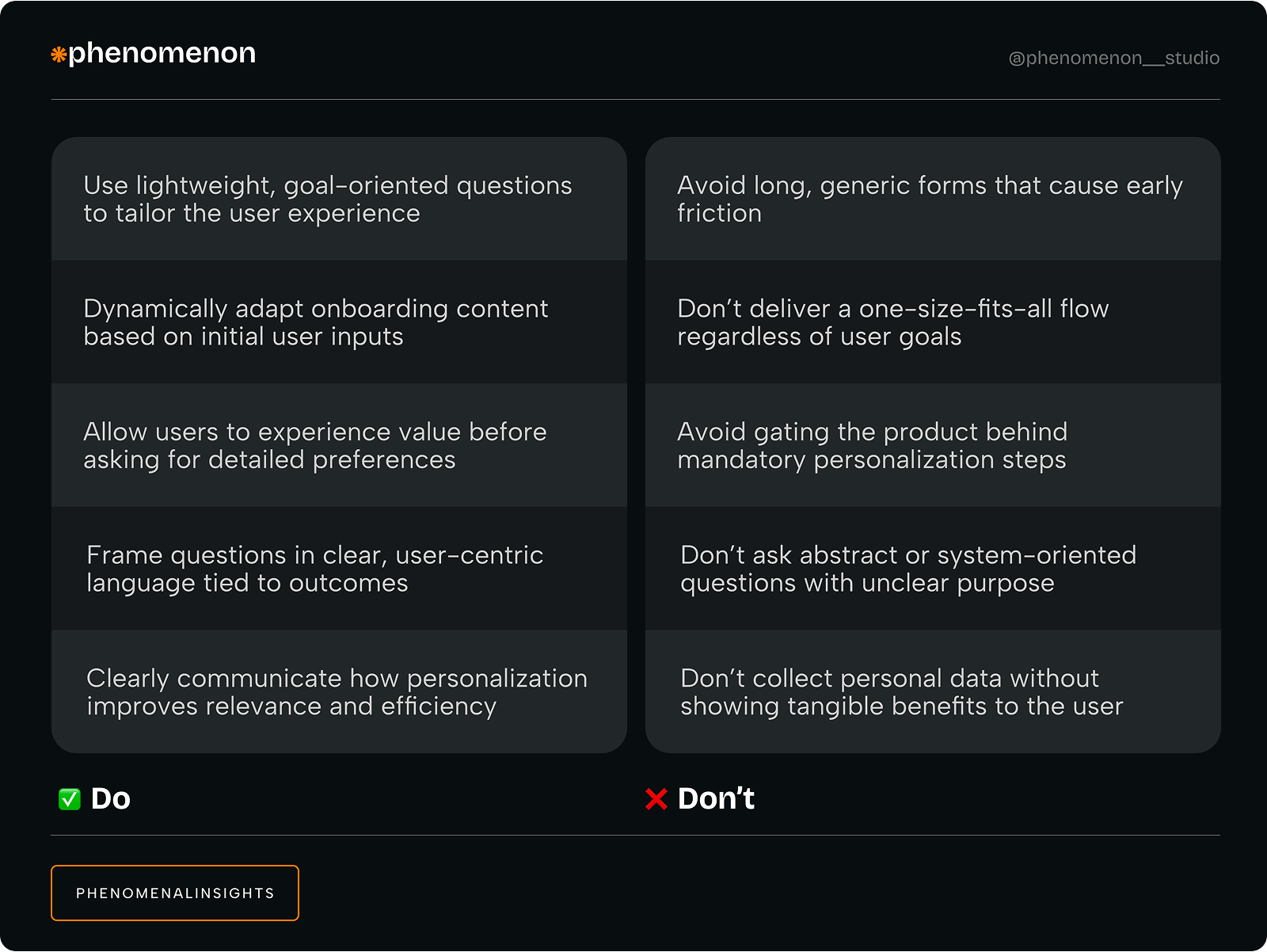

Personalized Onboarding – Aligning With User Goals

Personalization isn’t just for e-commerce. In FinTech, it helps guide users to the right tools for their goals — whether that’s saving for travel, sending money home, or investing.

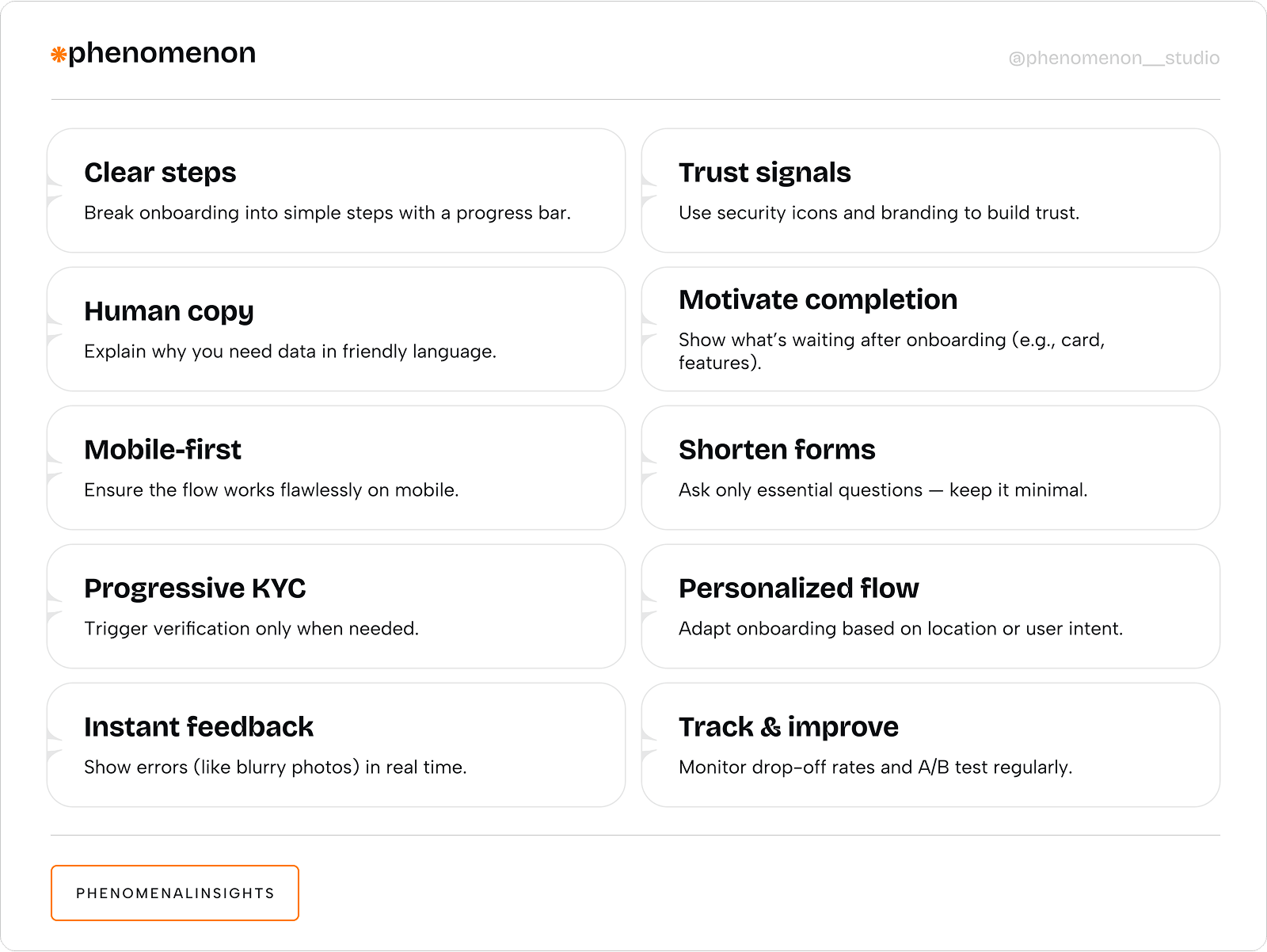

UX practices for FinTech onboarding that work

- Shorten & split: Replace long forms with a multi-step process. Show users one task at a time.

- Set expectations: Use microcopy to show how long things will take (“Takes ~90 seconds”).

- Gamify the flow: Use checkmarks, progress bars, and visual feedback to create a feeling of accomplishment.

- Trust signals: Add encryption badges, short privacy messages, and branded security visuals.

- Personalize: Ask only what’s needed. Use geolocation or previous behavior to adapt steps.

- Test relentlessly: Run A/B tests on onboarding variants. Measure activation, KYC completion, and time-to-first-transaction.

Why UX in onboarding = FinTech growth

Onboarding is your most leveraged moment. Every percentage point improvement:

- Reduces wasted CAC (Customer Acquisition Cost)

- Boosts activation rate

- Increases LTV (Lifetime Value)

- Lowers support costs

It’s not a design task. It’s a growth initiative.

UX isn’t just about how things look — it’s how they work, how they feel, and how users trust them.

Fast, friendly, and focused wins

When onboarding is designed with care, it can transform a hesitant visitor into a loyal, verified customer in minutes. When it’s not, it becomes a silent growth killer.

If you’re building or scaling a FinTech product, ask yourself:

- Are you making people feel safe, or overwhelmed?

- Are you respecting their time, or wasting it?

- Is your onboarding designed for humans — or for lawyers?

At Phenomenon studio, we use this 10-point onboarding checklist as a core framework when working with FinTech products. Whether we’re improving feature onboarding flow, optimizing time-to-value, or reducing user drop-off, this list helps us stay focused on what really matters: clarity, trust, and speed. It’s not just a guideline — it’s part of our process.

Invest in UX early. Because onboarding is not the beginning of a journey — it is the journey.

Share this opening with friends

Mar 25, 2026

7 min read

Explore expert UX/UI design services in 2026 — from accessibility compliance and AI interfaces to pricing benchmarks and sustainable UX. Learn how Phenomenon Studio delivers results.

Mar 24, 2026

9 min read

UX consulting services that scale with you. Partner with a results-driven UX design consulting firm for expert guidance—from product discovery and design systems to dedicated teams. Trusted by leading UX consulting firms.

Have a project in mind?

Let's chat

Have a project to

discuss?

discuss?

Have a partnership in

mind?

mind?